Money Debasement: A Plain Fact

Debasement is a simple act: taking away from the worth or quality of currency. It’s an old trick, dating back to when coin-makers scrimped on gold and silver, slipping in lesser metals but pretending nothing had changed. Nowadays, debasement hides in the guise of increased money supply, which chips away at the value of your cash.

Kings and emperors, they all did it. Back when money was gold and silver coins, they ordered their banks to shave the edges of each coin and use the filings to make new coins. Other techniques included punching a hole in the center of each coin, and then heating the coins enough to close the gap.

Today, central banks have a few different ways of increasing money supply, one of the most popular is to buy government debt, which is known as Quantitative Easing (QE). It works like this: the government issues debt in the form of notes, or government bonds, which is a promise to pay back the holder plus interest, often in the form of regular payments throughout the bond’s duration. The central bank buys these bonds at the market rate and puts them on their balance sheets as assets. From these assets, it can create money as liabilities or claims on its balance sheet.

Essentially, the newly created money is “backed” by the government’s promise to pay back the value of the bond. In this way, the supply of money is increased and when this process is undertaken excessively, the purchasing power of the currency declines.

QE allows governments to increase their funds without raising taxes but the result is a quiet, steady dilution of the currency's value. However, if the funds raised from bond sales are invested wisely and used to grow the economy, then the debasement effects could be offset by higher GDP. However, the risk is that the economy doesn’t grow enough and the government then must issue even more debt to pay off the original debt, which would be like using a second credit card to pay the overdue balance on your first. Alternatively, they could cut spending and raise taxes and force austerity on the population for the greater good — not a popular strategy.

On the other hand, there are some who don’t see this as an issue because they argue that government debt is valuable enough to back a currency. US government debt is popular because the US is very rich and has never defaulted on its obligations. So, for some, this is a good enough base from which to issue fiat money.

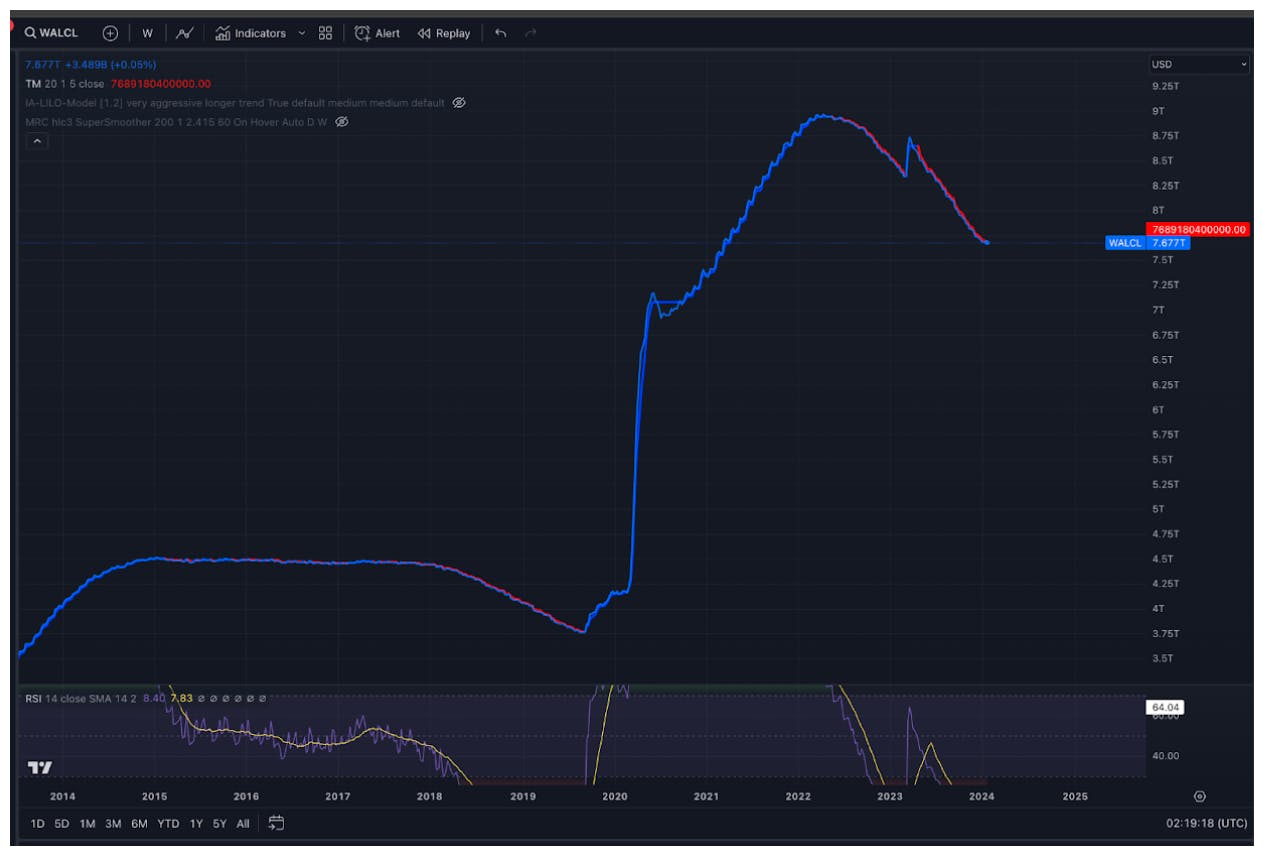

However, governments have a history of over-using their borrowing privileges. Due to the economic shocks of the last decade, we have gone through a period when central banks used QE to keep interest rates artificially low. As seen from the graph above, depicting the Federal Reserve’s balance sheet, QE took off as a way to deal with the recession that followed the Great Financial Crisis in 2008. They were just starting to taper off their liquidity injections when COVID hit and they were forced to ramp up the use of the Fed’s balance sheet to record levels. If they hadn't done this then the economic response to both those crises would have been much harsher, but the consequences have left us in the dangerous situation where the future GDP of most advanced economies may not be able to cover government debt payments. Also, debasement leads to inflation. And, while a cheaper currency might help exporters, rising prices places a heavy burden on consumers and savers.

Inflation is different to debasement because there are other factors at work. Debasement is the first domino and inflation falls further down the line. The main question is how much prices will increase.

For example, the price of tomatoes is a decision taken by the shop owner and will depend on supply chains, harvests, and what his or her competitors are charging. Inflation can also be artificially high due to monopolistic enterprises using an increase in money supply to pump their prices beyond the fair value.

Debasement affects the whole economy all at once, because the currency is devalued at the source, but inflation’s impact is scattered. Due to myriad factors that weigh on the price of goods and services, inflation may rise in some sectors, but not others. For example, if there’s a big forest fire then the price of lumbar might rise, followed by the price of new houses, but food prices might be unaffected.

Another aspect of this process is that debasement can seem to wax and wane. For instance, during the 1990s to 2010s, a significant event occurred: the globalization era. This period saw a vast, previously untapped labor force from China and other regions integrate into Western capital markets and corporate structures. The result was a broad suppression of both prices and wages. However, as China’s economy changed in recent years, it was no longer able to counterbalance the ceaseless money creation by the world’s advanced economies and the effects of debasements are once again asserting themselves.

Some economists argue that a little debasement can work in a country’s favor. For example, a weaker currency can make a country's exports more competitive in international markets, leading to an increase in export volumes. Furthermore, by making imports more expensive, a debased currency can encourage domestic consumption of locally produced goods and services, which can stimulate the economy.

Because we have had a sudden and large debasement of our currencies over the last decade, hard assets have increased in nominal value because there’s more of the denominator sloshing around. Let’s take Hong Kong property. The island isn’t getting any bigger so land is at a premium. Over time, like many important cities, landlords divided their properties into smaller units to gain more tenants, but eventually there comes a point where you can’t fit any more people in. So we can say Hong Kong property is a hard asset because there is an ultimate limit to the amount of units you can fit onto the island.

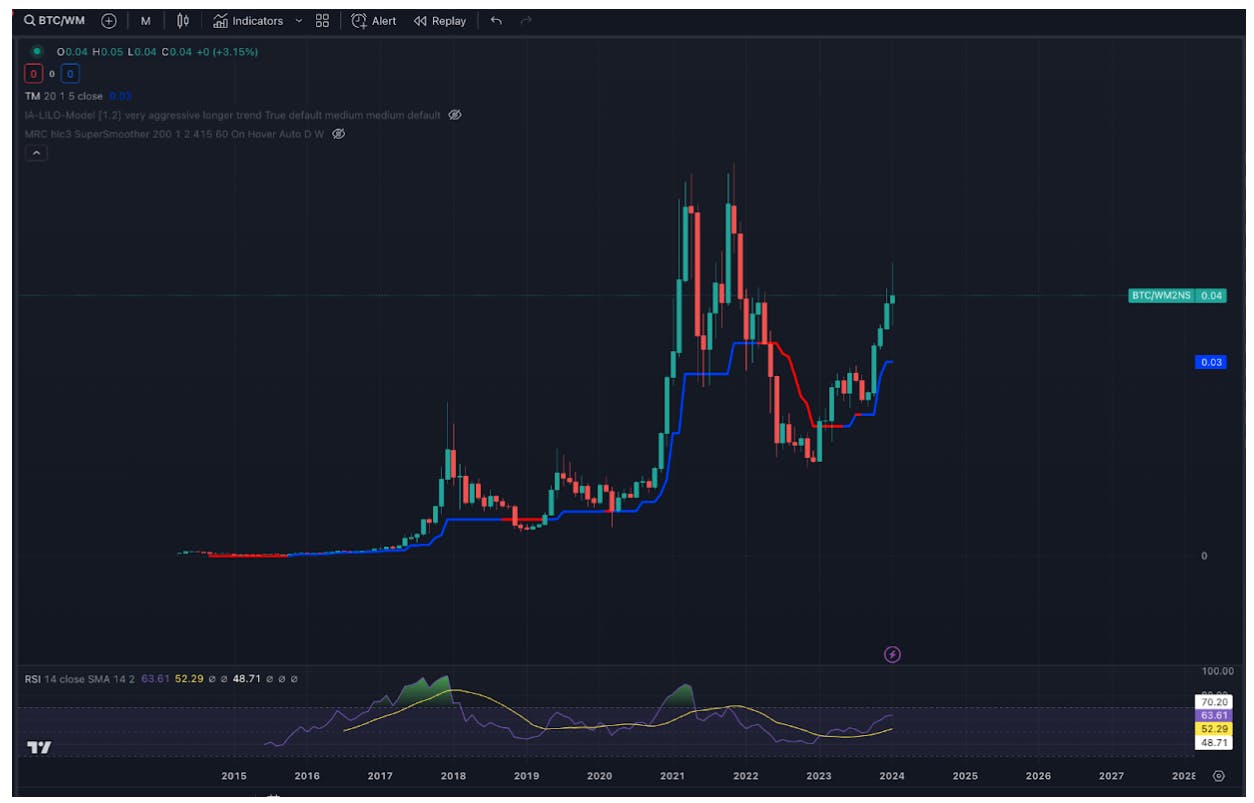

Bitcoin is another so-called hard asset because it can’t be debased even slightly. Its cap is programmed to be 21 million coins and no more can be created. This is why some call it “digital gold” because, like gold, there’s a limited supply and people use it for speculation and as a store of value. The main difference is that Bitcoin is new, which comes with risks and opportunities. On the one hand, it’s untested whereas gold has a long history, but on the other, it’s still small and its price could grow much higher than gold if it is widely adopted.

History’s full of empires and nations that saw their money crumble through debasement. Roman emperors, Ottoman sultans, English kings, all have played the game and lost. It's a lesson written in the ruins of coins and economies, a warning to those who would follow in their steps.

However, Bitcoin stands apart. Capped, coded, it cannot be swayed by the will of the few. It's money made by many, owned by those who choose it, and a possible heir to the throne of gold.

Disclaimer: The information contained in or provided from or through this article (the "Article") is not intended to be and does not constitute financial advice, trading advice, or any other type of advice, and should not be interpreted or understood as any form of promotion, recommendation, inducement, offer or invitation to (i) buy or sell any product, (ii) carry out transactions, or (iii) engage in any other legal transaction. This article should be considered as marketing material and not as the result of financial research/independent investments.

Neither SBorg SA nor its affiliates (“Entities”) make any representation or warranty or guarantee as to the completeness, accuracy, timeliness or suitability of any information contained within any part of the Article, nor to it being free from error. The Entities reserve the right to change any information contained in this Article without restriction or notice. The Entities do not accept any liability (whether in contract, tort or otherwise howsoever and whether or not they have been negligent) for any loss or damage (including, without limitation, loss of profit), which may arise directly or indirectly from use of or reliance on such information and/or from the Article.